Four and a half years ago, at the national conference of the AWU in 2013, general secretary Paul Howes issued a warning:

Four and a half years ago, at the national conference of the AWU in 2013, general secretary Paul Howes issued a warning:

- Howes warned that unless some gas was reserved for domestic use, and limits on coal seam gas extraction were lifted, the massive investment boom in LNG would soon affect the supply and price of domestic gas. And consumers, business and manufacturers would all suffer.

“This is one of the most important resolutions we’ll debate at this conference,” he said.

He added:

- “It is bizarre that this country has gone through a massive expansion of natural gas right across every state and yet we can’t seem to keep any of this gas, to add value here.”

Philip Coorey at the AFR reports that Howes received support from such well-known ratbag socialists as the Australian Industry Group and Dow Chemical boss Andrew Liveris.

Howes now scratches out a living at KPMG. Martin Ferguson, resources minister at the time, who now chairs the Advisory Board to the Australian Petroleum Production and Exploration Association (APPEA), was not impressed. While he agreed on lifting the limits to CSG extraction, he claimed that a gas reserve would “deter the very investment needed to deliver more gas to the domestic market”.

- Howes berated Ferguson, arguing he “should be there talking about what resources can do for this country, not for the companies that extract them in the first place”.

Of course, Turnbull now blames Bill Shorten, who at that time was probably Minister for Employment and Workplace Relations and Minister for Financial Services and Superannuation and new to cabinet.

Labor did take a proposal for a form of gas reserve to the last election, and was slammed by the Coalition as being protectionist.

Labor energy spokesman Mark Butler says at the time gas companies gave assurances that they would not drain domestic gas supplies to fill export contracts and that domestic gas would cost the same as the Asian price. He says they lied.

Butler puts the story in this Lateline interview with Emma Alberici. The price was always going to go up to export levels when we started exporting, that’s Economics 101. Then the companies assured Labor that domestic supplies would not be affected. When they were Labor took a gas reserve policy to the election, but was criticised by Turnbull for sovereign risk and being economically irresponsible.

The government is still concerned about sovereign risk although Giovanni Di Lieto of Monash University explains in some detail why it is not an issue in this case. Labor prefers to pull the regulatory trigger set up by the government, saying only this can provide the certainty needed. The government has done a deal short of regulation with the main suppliers who have promised gas for the domestic market for the next two years.

The companies say that in fact there has never been a shortage – they have been supplying gas beyond their contracts to the Asian spot market, which itself is essentially over-supplied.

- Ian Macfarlane, a former federal resources minister turned Queensland gas lobbyist, said Queensland’s gas exporters would offer to sell it back to Australia’s domestic market for the LNG netback price – under $10 per gigajoule – but domestic buyers had to guarantee they would buy it by signing contracts.

The so-called “LNG netback price” is the Asian spot market price, less the cost of getting it over there.

His call for contracts relate to the fact that buyers of gas have been holding off to see what happens with government action. Angela Macdonald-Smith in the AFR points out, however:

-

as one buyer ominously pointed out, the electricity forward price in the eastern states edged up $2 a megawatt hour on Wednesday afternoon after the gas deal was announced.

That would signal that those in the know anticipate gas prices will be higher than they might have been under the Domestic Gas Security Mechanism, not lower.

The ACCC has come up with benchmark prices, but suppliers say they can’t supply at the marginal cost of production. Macdonald-Smith:

- Today’s price offers for gas to industrial customers of $10-$16 a gigajoule are a world away from the “benchmark prices” quoted by the Australian Competition and Consumer Commission of $5.87 in Queensland and $7.77 in Victoria.

Gas and petroleum exploration and the production, treatment and marketing of natural gas, crude oil, condensate, naphtha and liquid petroleum gas; transportation by pipeline of crude oil.

In reality, prices much closer to the $10 mark are probably the best major Victorian manufacturers can expect, with smaller users a little higher.

LNG sources in Queensland quote about $6 a gigajoule for a marginal cost price from the “dry” – and so expensive – gas extracted from coal seam gas seams in the state, which has become the dominant source of available gas on the east coast.

When up to $3.50 a GJ of transportation costs to the south are added, the total still looks out of reach of some manufacturers.

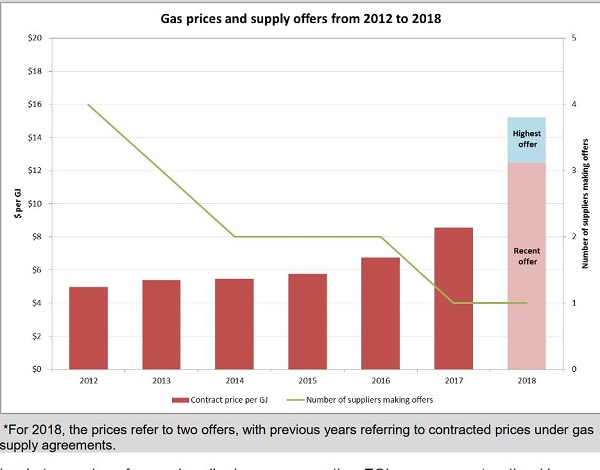

This graph from the ACCC report shows a distinct lack of competition:

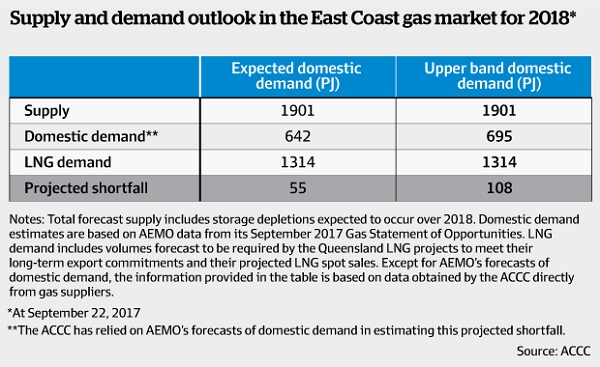

ACCC are assuming a shortfall of 55 to 108 PJ in 2018 as forecast by AEMO, from Macdonald-Smith again:

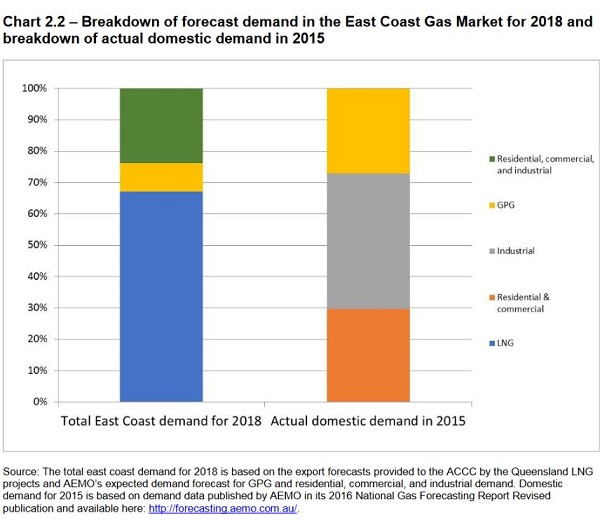

From the ACCC report, domestic demand is shown as follows:

Blue in the first bar represents LNG. GPG (gas-powered generation) is yellow in both bars. The green of the first bar subdivides in the second into grey for industrial, and orange for residential and commercial.

The most difficult to forecast is the gas-powered generation because of the intermittency of its use.

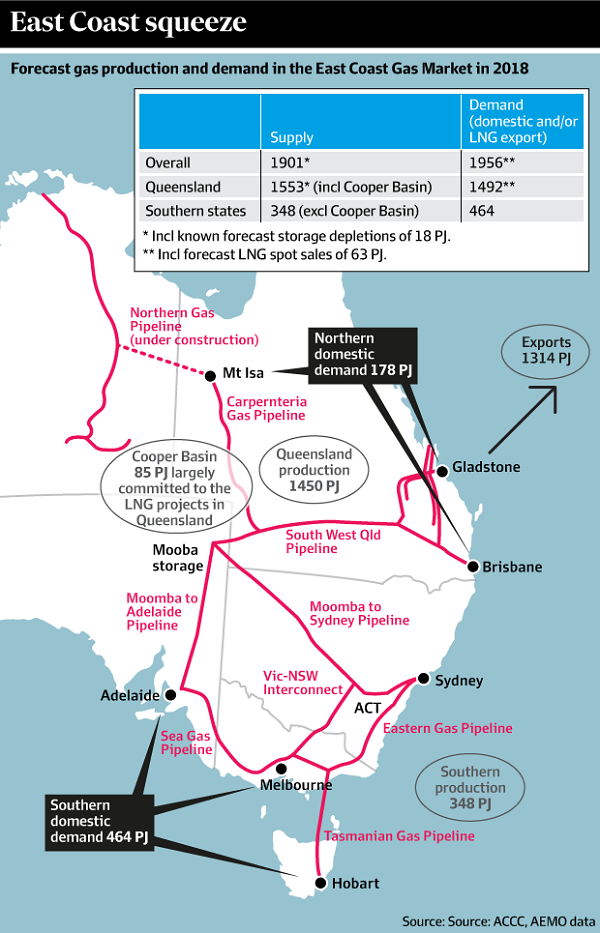

Gas producers say they have the shortfall covered, but then their long-term LNG contracts also include increased supply. Before we identify where this may come from, I’ll put up the phantasmagorical map in the ACCC report, as per the AFR version:

First, a pipeline connecting Tennant Creek and Mt Isa is already under construction, to be completed in 2018. If the NT removes its fracking ban (unlikely) more gas could be sourced there.

Second, at the other end, AGL plans to build a gas import hub at Crib Point on Mornington Island.

Third, I heard that Queensland has now written to Malcolm Turnbull proposing a gas pipeline directly from the Bowen and Surat basins to NSW and Victoria. Turnbull seems to regard the Palaszczuk government as a caretaker government, so I’m sure he’ll ignore the request.

Fourth, Queensland has just issued its annual resource exploration program and has granted approval to at least one new coal seam gas venture.

Fifth, according to Matthew Stevens in the AFR Santos is still progressing its Narrabri CSG project, currently valued at zero on its books. Stevens says no actual fracking is required, and the proposal is to sink diagonal rather than vertical wells, so that multiple wells can be sunk from one point with less surface disturbance. The cost of sinking such wells has now fallen from $3.2 million to $900,000 each.

However, all I can find elsewhere in the media is written by the likes of the Wilderness Society, hell-bent on stopping it.

Mark Ludlow in the AFR reports that Santos plans to drill up to 850 wells on 425 sites on the 95,000-hectare project area, mostly on private land with the agreement of the landholder who will be paid compensation. They submitted a 7,000 page EIS earlier this year, which evoked a record 23,000 submissions but only 500 submissions from the local area. Only 300 submissions most of them local supported the project.

It could supply about half NSW’s gas needs, with gas flowing from 2019-20. However, it is expected to remain in regulatory quicksand for at least another two years.

Turnbull’s calls for change to CSG development have been rejected by the states.

Sixth, Santos has engaged in gas swaps to make available gas to the domestic market. There is a credible story that the built the second gas train at Gladstone when they did not have enough gas to supply it.

Matthew Stevens back in April explained the Santos in fact owns the gas crisis. Essentially it bargained on the oil price staying above $70 per barrel. Also it assumed that CSG development in NSW would go ahead. Moreover, its own CSG ventures in Queensland have underperformed. Now it finds itself contracted to supply gas overseas cheaper than the price it could get in Australia. As 30% owner and operator of the GLNG joint project with three multinationals it now supplies the local market by doing swaps with its international partners to meet the overseas contracts.

Which of course affects the viability of its second train in Gladstone.

The whole new deal struck this week is still a work in progress, with a further meeting next Tuesday. There has been a suggestion that a gas-buying entity be set up by the government, so that the risk would be shifted to the tax payer.

The government as gas trader to keep the lights on. Surely not!

Update:

There is talk in the AFR of the Commonwealth Grants Commission penalising states that don’t develop their gas resources.

There is a precedent in that Western Australia is assumed to earn money from pokies in venues other than casinos, although WA has forbidden such pokies.

In other news, James Fazzino, outgoing CEO of Incitec-Pivot, has been warning about Australia’s looming gas train wreck for the last six years. In 2013 his company spent a billion dollars on an an ammonia plant in Louisiana. When he wanted gas there he had 50 companies bidding to supply.

One of his last tasks will be trying to secure gas for Incitec’s Gibson Island fertiliser plant in Brisbane. This will hinge on the Queensland government’s gas reservation strategy, which business supports, a stark contrast to the way the NSW and Victorian governments have dealt with energy policy.

Fazzino is leaving his job as CEO to become chair of Manufacturing Australia, although there may not be much to chair unless we sort out gas and electricity.

Brian

Crib Point is on the coast of the Mornington Peninsula, which lies between Port Phillip Bay and Westernport Bay, near Melbourne.

Crib Point has a deep water port in Westernport Bay.

It’s near the town of Hastings, which has some heavy industry.

The Govt as gas trader?

Here in Victoria a few decades ago we had a (wait for it) “Gas and Fuel Corporation” !!! The State Govt owned it, as far as I can recall.

I’m old enough to remember the COR, Commonwealth Oil Refinery (???)

and we did all that without a Stasi or KGB.

Yes, we had TAA, the Commonwealth Bank, Commonwealth Serum Laboratories etc.

We could do worse, but you would not expect it from the Liberals.

Bass Strait is running low on gas, according to the Fin Review.

Yes, Brian

I would not expect it from the Liberals.

The PM must be listening very hard to focus groups annoyed about rapidly rising power and gas prices.

Climate policy is making some unexpected “bedfellows”* these days.

* NOT a reference to marriage.

There is talk in the AFR of the Commonwealth Grants Commission penalising states that don’t develop their gas resources.

There is a precedent in that Western Australia is assumed to earn money from pokies in venues other than casinos, although WA has forbidden such pokies.

In other news, James Fazzino, outgoing CEO of Incitec-Pivot, has been warning about Australia’s looming gas train wreck for the last six years. In 2013 his company spent a billion dollars on an an ammonia plant in Louisiana. When he wanted gas there he had 50 companies bidding to supply.

Fazzino is leaving his job as CEO to become chair of Manufacturing Australia, although there may not be much to chair unless we sort out gas and electricity.

The real question is how much of this gas is really needed? For example:

-Residential and, I suspect, commercial gas could be replaced by renewables.

-Gas for power consumption could be replaced by renewables.

Hard to say for industrial without knowing more details. Gas is feed stock for a number of processes like fertilizer production and may be better for some types of heating compared with electricity. However, keep in mind that a whole range of of products that use natural gas as feedstock could be produced by processes that start with renewable electricity, water, air and, in some cases CO2.

Perhaps the question posed by this post should have been something like: “What could we do if we know the supply of domestic gas is going to be used up within 10 yrs?”

Asking where we are going to get the gas we think we are going to need limits our thinking.

John, as well as Chief Scientist they should have a position for Chief Lateral Thinker.

Brian: Asking the dumb and challenging questions is a key step in lateral thinking. Far too often we get trapped into answering questions that are too limited or keep the conversation stuck on the world view of particular professions. (Think economists and their predilection for seeing manipulation of prices as the only way to make things happen.)

I wouldn’t mind if the Lateral Thinkers were tucked away in the quiet, modest background.

They might do better than some of the shallow show ponies who prance around our public sphere. Yes, looking at you Mr Tim Flannery.*

* ref to his recent silly “Catalyst” session on ABC television.

Ambi: I have found that lateral thinking is a lot more satisfying when you have the power to make things happen.

Indeed

I’d be happy if every Ministerial office and every political party policy group had intelligent, experienced lateral thinkers.

The Minister can be accountable to voters. The party can offer its ideas yo the public. The lateral thinkers don’t need to be public figures.

Their suggestions and ideas can be thrashed out by the public.

Brian &

John Davidson,

On Friday’s (September 29) ABC-TV 7pm NSW News edition, in the Finance segment presented by Phil Lasker, was highlighted a recent report by Wood Mackenzie, that indicates Australia’s east coast gas prices will never return to those of a few years past. Extraction costs of new gas projects, particularly CSG in Queensland, are significantly more than legacy ‘conventional’ gas supplies that are now declining.

ABC.net.au analysis article headlined Gas prices: Deal done but days of cheap gas are long gone, updated 29 September 2017, by business reporter Stephen Letts, provides a more detailed similar report.

BP Statistical Review of World Energy 2017 indicates that in year-2016, USA was:

* ranked the world’s largest gas producer, at 21.1% global share;

* ranked the world’s largest gas consumer, at 22.0% global share; and

* held the world’s fifth largest gas proved reserves, at 4.7% global share; BUT

* its reserves-to-production was only 11.6 years.

If these figures are correct, and I see no compelling evidence to contradict BPSRoWE-2017 gas data, then it appears to me that a little more than one-fifth of year-2016 global gas production is likely to be heading into a sustained decline soon. And I think we will then be heading into a post- ‘peak gas’ supply world, with consequent further rising gas prices.

The Alternative Technology Association’s November 2014 report Are we still Cooking with Gas? highlights that based on current price forecasts and appliance price and performance trends, there are many cases where gas appliances are no longer the most affordable option for households for heating and cooking.

I concur with the ATA report’s findings, based on my first-hand experiences; by replacing my ageing gas hot water storage system in 2015 with a heat-pump hot water storage system operating during the day utilising rooftop solar-PV energy whenever possible, and retiring my living area gas space heater before last winter and installing a 4-star reverse-cycle air conditioner; to achieve substantial energy bill savings, with no detriment to lifestyle. Once I replace my sole remaining gas (oven/griller/cooktop) appliance with an electric (oven/griller/induction-cooktop) unit, then I can disconnect my house from the gas network and eliminate the steadily growing (and I think no longer trivial) gas network charges.

Apart from industries using natural gas as a feedstock for manufacturing plastics, artificial fertilisers and explosives, etc., I think there is no economic justification in the medium- to long-term to continue utilising gas.

We live in interesting times.

Geoff Miell, the above comment was again caught up in moderation, for no apparent reason, as it had no links. I can only think it was the device used for dot points, which the spam software may have regarded as suspicious!

The Fin Review reported yesterday that Asian spot gas markets spiked simply because of the prospect of Australian LNG being withheld.

I have another problem with gas. From the post Gas has got to go:

Moreover, methane is included in the climate models as, I believe, 23 times more potent then coal. In fact that is after 100 years. It starts in the first year at over 100 times. Here’s the graph:

To all,

Yesterday, BZE published on YouTube a video of their Discussion Group session conducted at Melbourne University on Monday, October 16, titled A Short-lived Gas Shortfall.

Beginning at time interval 0:1:40, Tim Forcey, a Melbourne-based energy advisor, outlines Australia’s gas supply outlook, uncertainties, and costs. I think he does an excellent job of putting an up-to-date perspective of Australia’s gas supply future.

From time interval 0:34:35, Dylan McConnell, who’s an energy analyst/researcher at the Australian-German Climate and Energy College, outlines the relationship between gas and electricity generation. He makes some key points beginning at time intervals:

0:43:28 – Gas and climate change;

0:47:02 – Gas vs RE – electrical-energy production

0:49:32 – Electrical energy cost comparison

0:50:55 – Gas vs electricity storage (and demand response)

0:55:22 – Energy storage (and demand response) – Lazard 2015

0:56:44 – Putting it all together

From time interval 1:02:55 there is a Q&A session.

The audio is not the best so you may need to concentrate to comprehend but the presentation slides are clear.

https://www.youtube.com/watch?v=_ORn3HywW1g