Recently John Quiggin in The fossil fuel crash of 2014 asked what should we make of the fact that oil prices have fallen from more than $100/barrel in mid-2014 to around $60/barrel today? He also looked at coal, I’ll stick with oil. Quiggin poses the questions:

The big questions are

(i) to what extent does the price collapse reflect weak demand and to what extent growing supply

(ii) will these low prices be sustained, and if so, what will be the outcome?

Quiggin says:

The answer to the first question seems to be, a mixture of the two, with some complicated lags.

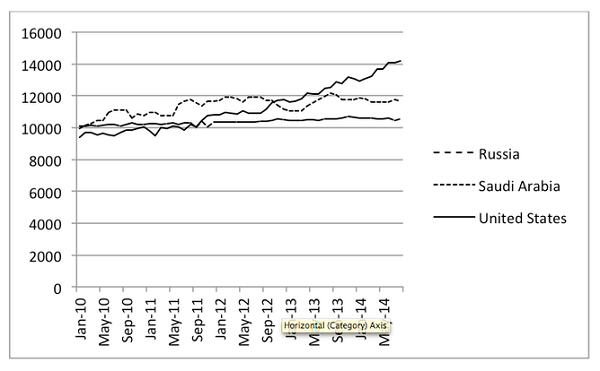

I thought it was the Saudis increasing supply to put the American frackers out of business. This turns out not to be the case. Richard Heaney gives us this graph on monthly oil production:

So it is the Americans who have largely increased supply. The Saudis have simply decided not to reduce supply, the usual tactic to increase the price. I’m sure they are hoping the American frackers will feel the squeeze.

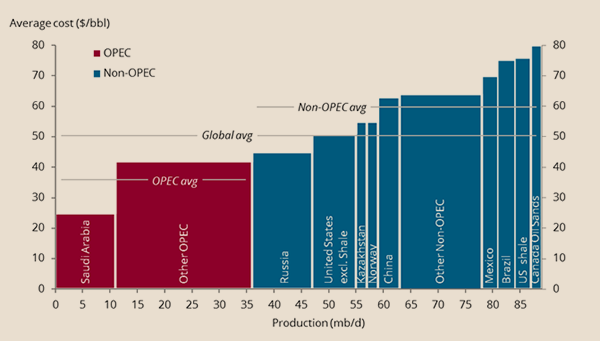

Anjli Raval gives this graph of costs:

Raval says that most at risk are the Canadian oil sands, US shale plays and other areas of “tight oil”. Also vulnerable are Brazil’s deepwater fields and some Mexican projects. Crude at $70 puts at risk projects for 2016 to the extent of 1.5 million barrels per day.

Raval has perhaps the best discussion of what might happen in the future. The short answer is that we don’t know. A pull-back in investment could lay the basis for the next price surge. There may also be a switch to cleaner energy sources.

Much of the discussion, including a Financial Times editorial arguing that the fall in the price of oil was good for the economy (the concern was over deflation), ignores climate change.

John Quiggin says, inter alia that:

if we are to reduce emissions of CO2, a necessary precondition is that the price of fossil fuels should fall to the point where it is uneconomic to extract them.

I’m confused. I thought the aim of carbon pricing was to make fossil fuels more expensive to discourage use and to make the use of renewable alternatives competitive.

Adair Turner in a piece Please Steal Our Fossil Fuels goes into considerable detail about the transition to renewables. If all the fossil fuels were stolen we would not be stuck (or not for long) and it would in the long run cost a negligible amount more. However, the assumption is that the transition will depend on price. Unfortunately electric cars may not be cheaper until the late 2020s. There is plenty of oil in the ground and whilst it is available we will keep using it.

Turner says “we should commit to leaving most fossil fuels forever in the ground” and no great harm would befall us economically if we did, but we won’t. Miracles would be required.

At this point I’ll state my case that we should act out of policy, not rely on markets or miracles. If Germany can forswear nukes because they are dangerous and evil, why can’t we do the same in relation to fossil fuels, which are even more dangerous? Sooner or later we’ll have to ignore the fossil fuel mafia.

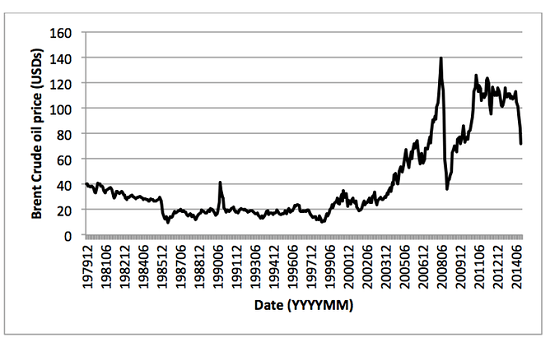

Before I go, Heaney has this graph of the oil price in recent years:

It demonstrates that oil can be extremely volatile. There is no way of telling where the current crash will end, but my guess is that it will more or less stabilise soon. After that we are in uncharted territory.

Elsewhere Jeffrey Frankel makes several interesting points.

Firstly most dollar denominated commodities have fallen in price, including iron ore, silver, gold, platinum, sugar, cotton and soybeans. So something general is going on beyond the vagaries of specific commodities.

Secondly, The Economist’s euro-denominated Commodity Price Index has actually risen over the last year.

Third, and most importantly, it seems, there is a link between commodity prices and interest rates. When interest rates go up, commodity prices fall. Frankel suggests that traders are anticipating a rise in interest rates in the US next year. It’s not the whole story, but perhaps an important factor overlooked elsewhere.

The current cuts in oil price will put a hold on new exploration and development. Which is likely to lead to higher price spikes later on.

Many oil consumers will want to be less dependent on ME oil or exposure to volatile oil prices.

There are a lot of good reasons for reducing oil consumption.

Watch this space.

On the point of confusion, the necessary condition is that the price received by producers should be below the cost of production. One way to achieve this is a tax that raises the price paid by consumers to the point that demand falls, and drives down the net price received by consumers.

Don’t you mean producers ?

John Q: We have been running a real life experiment in Australia on the effect of petrol price on consumption. The results suggest that the whole thing is pretty price in-elastic. Increasing fuel prices have had little effect on consumption. Hardly surprising given that people would consider keeping the car going as an essential and, in Brisbane at least, driving an already owned car is much cheaper than using public transport.

If we seriously wanted to reduce fuel consumption we might try using offset credit trading to drive down the average fuel consumption of new vehicles.

On reflection I can see two contrasting scenarios. The first is the ‘unmodified market scenario’.

As prices fall, consumers may use more fuel. Producers exploit cheap resources first. As time goes by more and more expensive fuel comes onto the market until eventually renewables become competitive.

Under the second scenario, a price is put on carbon. Consumers may use less fuel, but the point where renewables are competitive is reached sooner because of the added carbon price.

In both cases the main factor is the price competitiveness of renewables.

Beyond that a variety of policy actions could be taken to change behaviour. First, emissions levels could be mandated for new cars with offset trading credits as suggested by John D.

Second, a cap and trading system for carbon pricing would send a strong signal to investors that there is risk in expensive oil resources, especially if the caps are designed, say, to reach zero emissions by 2050.

Third, we could construct public transport infrastructure powered by renewables.

With coal we should mandate that no new coal power stations are built and that decommissioned ones stay decommissioned. Further we should have an active policy of taking coal-fired power out of production.

I’m sure there are other policy ideas out there, but I’m arguing that price competitiveness, even with carbon pricing unless it’s savage, won’t get us there fast enough.